FUNDRAISING FOR FEMALE FOUNDERS SURVEY RESULTS

Introduction

As more women enter the entrepreneurial landscape, it has become increasingly important to understand the unique challenges they confront while building and scaling successful businesses. In response to this, Pink Salt Ventures has carried out an in-depth survey involving 90 female founders to gain deeper insights into their experiences and perspectives within the ecosystem. Our findings, both eye-opening and enlightening, expose an array of issues that female founders face, from securing adequate funding to navigating expectations for financial projections. Moreover, the study sheds light on the prevailing perception among female entrepreneurs concerning a lack of understanding of what constitutes a VC-backable business.

We developed our questionnaire in partnership with Dana Kanze, Assistant Professor of Organizational Behaviour at London Business School. The TED talk about Professor Kanze and her co-authors’ published academic research on gender bias in investor Q+A is a must-see.

Key Insights

An overwhelming 97% of female founders agree there is a fundamental difference between how male and female founders are treated.

Female founders view the lack of female decision-makers in venture capital as the largest barrier to funding, especially at later stages, with 83% of Seed+ founders surveyed citing this as a barrier to funding.

Female founders view the fundraising process as arduous, with those surveyed providing a 4/10 average rating of their experience getting to a term sheet.

Female founders exhibit a preference for pitching their best-case scenario projections (56% of the sample), but a sizable amount (44% of the sample) express a tendency to rely on risk-adjusted projections.

82% of female founders are first-time founders, with a small minority of serial entrepreneurs (18%). Out of the serial entrepreneurs, 88% choose to start with a team (vs. as sole founders), compared to 58% of first-time founders.

Even at the earliest stages of founding a company, 76% of female founders expressed a lack awareness of what fundamentally constitutes a VC-backable business.

Founder Experience

The majority [97%] of participants agree that there is a significant difference in how male and female founders are treated. This majority assertion is paralleled in participants’ reported experience interacting with venture capitalists according to gender, with 73% of female founders noticing a difference when pitching female versus male VCs. Data also revealed that the lack of female decision-makers at VC funds represents the most significant barrier to funding. Broken down by funding stage, 83% of Seed+ founders identify this as a hurdle to securing capital, while 71% of Pre-Seed founders cite this as a major obstacle.

Contextualising the funding barriers, female founders report venture capitalists’ insufficient understanding of the problems and markets they are addressing as the second largest roadblock to them getting funded. These disparities speak to powerful external and internal factors that can influence a female founder's capacity to successfully attract funding, such as investor demographics, lack of investor understanding regarding the problem or market being addressed and differing approaches to projecting business potential.

As stated by Dana Kanze, “These results point to downstream effects as well. Until female founders receive the funds they need at the valuations they deserve, they won’t participate in the liquidity events that can enable them to become serial entrepreneurs and investors themselves.”

Pitching

When it comes to pitching their business projections, female founders show a modest tilt towards their best-case scenarios (56% of the sample), with a substantial fraction (44%) preferring risk-adjusted projections. Female founders also dedicate significant time to accurately valuing their companies, with 72% asserting no discrepancy between their estimation of their company's worth and that presented by the investor. This is reflected in the diligence process, as founders spend an average of 30 hours creating pitch documents before taking calls with VCs.

Even at the earliest stages of founding a company, 76% of female founders cited a lack of awareness of what constitutes a VC-backable business. Given these hurdles, 70% are interested in female-only acceleration, incubation, and boot camp programs to improve their business and pitching ability.

Fundraising

The survey results reveal the intricate and challenging landscape female founders encounter in the fundraising process. Notably, the funds secured by female founders differ considerably depending on their industry and business stage. The survey discovered that 50% of female founders raised capital within the £0k-250k and £1-5M brackets, with an even distribution across both ranges. This aligns with the European State of Tech report, indicating that in 2022, all-female teams obtained a median seed round size of $1.4 million, approximately 40% less than the $2 million acquired by all-male teams. This funding disparity is more pronounced at the Series A stage, where female founders raised only $7.9 million compared to $12.1 million raised by their male peers. The imbalance is further accentuated by the fact that female founders typically participate in more investor meetings yet receive less funding in comparison to male founders. These insights emphasise the importance of addressing the specific barriers faced by female entrepreneurs in accessing capital, as well as the need for tailored support mechanisms to overcome these obstacles.

The fundraising process is viewed as demanding by female founders, with respondents giving an average rating of 4/10 to their experience of securing a term sheet. This process appears to be particularly daunting for later-stage (Seed and Series A) founders who rated their term sheet experience lower than Pre-Seed founders. This distinction across stages could be impacted by the higher fundraising requirements, additional due diligence and proof of concept post-launch.

When faced with VC rejections, female founders cited issues like fundraising timing or that the stage of the company was too early. After rejection, 61% of female founders reported receiving generic feedback, whereas 28% received helpful feedback (of which only 5% received onward referrals). On the flip side, female founders provided reasons such as limited fit, network, and value add (or lack thereof), as well as bad or poor feedback from other startups, as reasons to say no to an interested VC. However, even after rejection, female founders value their relationships, with over 70% of founders stating that they keep in touch with their VC contacts for future opportunities.

Demographics

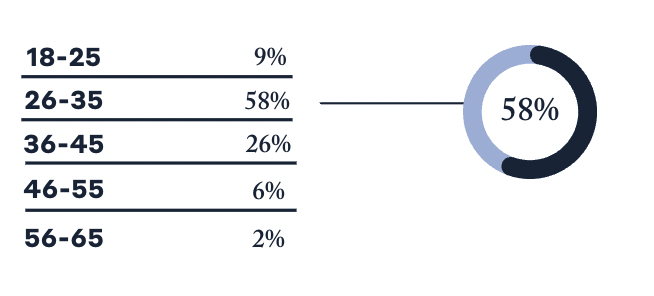

The majority of female founders surveyed were between the ages of 26-35, followed by founders between 36-45, which aligns with the global statistics indicating the average age of a female entrepreneur is 42 (Forbes). Interestingly, results reflected a skew towards younger founders, following the rise of Gen-Z/Millennial entrepreneurs post-pandemic.

Female founders surveyed were predominantly first-time entrepreneurs, while only 18% were serial entrepreneurs. This trend is reflected in Reg CF's study, which found that 63.5% of founders raising capital had no prior experience. For serial founders, 88% chose to launch with a team, suggesting that those with prior experience recognize the importance of working with experienced operators and are more likely to prioritize building a solid team from the outset.

Team composition was found to be crucial for female founders, with 38% of them starting their companies alone, while 62% launched with a team. Half of these founding teams were all-female, while the other half had diverse gender compositions, highlighting the value of diversity and support, particularly at the earliest stages of the entrepreneurial journey.

Takeaways For Founders:

The survey findings underscore that the onus for transformation does not lie with the female founders, but rather with the investment community. Nevertheless, as we work towards catalysing this shift, there are several strategic recommendations and useful resources that female founders may find helpful:

1. Pitch your best-case scenario

As female founders skew towards modest projections of their company’s potential, make sure to pitch an optimistic, data-driven representation of your business to remain competitive within the startup ecosystem and increase your chance of securing funding.

2. Find investor communities supporting female founders

The right angel investors can make all the difference in connecting you to wider networks and helping you navigate the complex fundraising landscape.

A few angel networks and programs we rate in the UK:

3. Build your network before you fundraise

Fundraising is a prolonged and arduous process, particularly at the later stages of building a company. Building a diverse network of VC backed-founders and investors can support you in securing warm introductions and alleviating the dependence on cold outreach.

One brilliant, supportive female founder network we can recommend in the UK is Founder’s Social, contact Tamta to get invited to the community.

4. Know what constitutes a VC-backable business

The results show there is significant confusion as to what business models and ideas can attract VC funding. Research how VC business models work and whether VC financing is right for you.

TLDR: you will want and need to have the ambition to grow into a £B+ Valuation and get to £100m Revenue in 5-7 years.

How do VCs make that judgement? The potential market needs to be there as well as the ambition and competence.

Why so big? Are VCs greedy? No.

VCs make a number of investments with the knowledge that only a handful or less will be big winners, some will fail, and some won’t make it big, see also Power Law Distribution. Every investment they make needs to have the potential to be a big winner. Hence, to be a VC-backable business, you likely need to +100x your entry valuation at a minimum to get early-stage VC financing.

This is ultimately the VC business model, which does make sense when financing innovation and technology where exponential growth opportunities exist. The high-risk, high-reward strategy makes sense for investors in VC funds because the returns beat the stock market over the long run. If they don’t then investors may as well put their money in the stock market.

And by the way, venture capital isn’t the only way to build a ‘successful’ business.

To cite this report, please use the APA format below:

Pink Salt Ventures. (2023). The Female Founders Report. Pink Salt Ventures.